Ways to Verify a Bank Account: Holder vs. Access

Before diving into the different verification methods, it’s crucial to understand the distinction between account holder verification and account access verification:

- Account holder verification confirms that the person or company is the legal account holder.

- Account access verification confirms that the person can access the account.

Key insight: Every account holder or authorized user has full access to their account, but not everyone with access is an account holder. Understanding this distinction is essential to choosing the right verification method for each use case.

Ways to Verify Account Holders

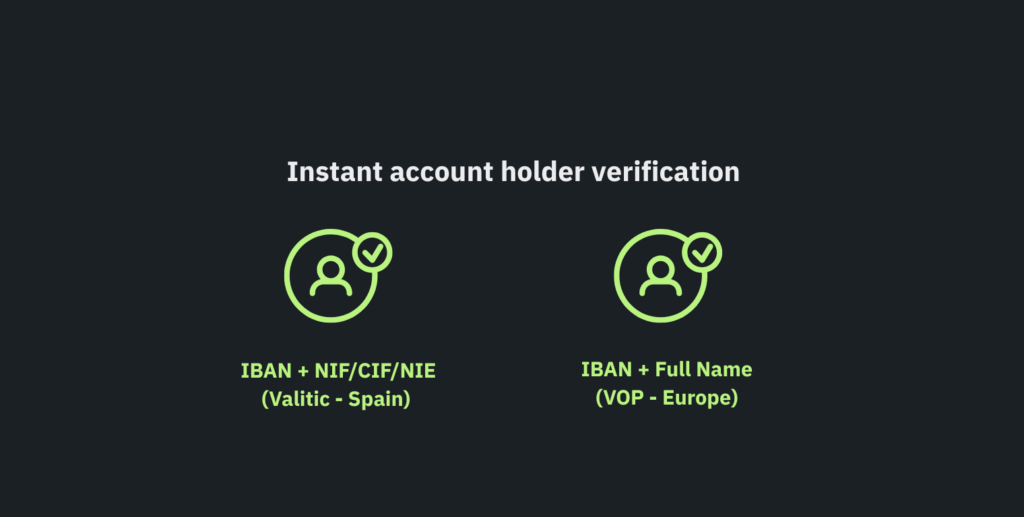

1. Instant Verification via Interbank Communication

This method involves directly consulting the user’s bank to verify that the provided information matches the official account data—without requiring any user intervention.

Available Technologies:

- Valitic: Available in Spain. Verifies IBAN-NIF match in real time.

- VoP (Verification of Payee): European standard available from October 2025.

- Other national alternatives: Each European country is developing its own systems.

Pros

- Instant verification (≈ 1 second)

- Seamless, frictionless user experience

- Maximum reliability: data comes directly from the bank

- Compatible with over 99% of Spanish accounts (Valitic)

- Full SEPA coverage (VoP)

Cons

- Limited availability depending on country/region

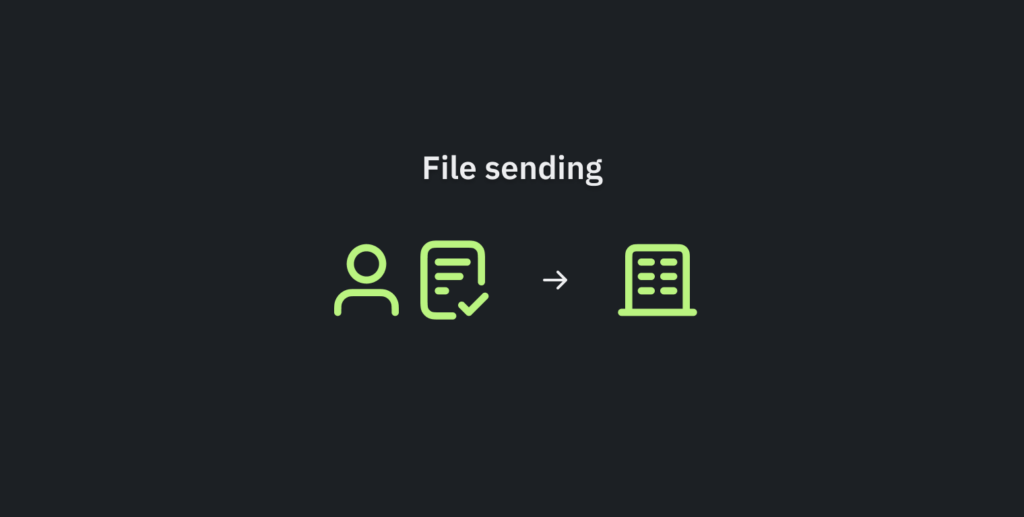

2. The user provides a bank statement or certificate

This method consists of asking your users to provide a bank statement or certificate issued by their banks with their name and bank account number shown.

Pros

- This method is quite trustworthy since your customer’s bank account is issuing a certificate.

- It’s also not expensive in terms of technology required from your side.

Cons

This method has two main drawbacks:

- It’s performed outside your web process (the users need to go to their online banking). You will lose track of your users’ activity and if they decide not to send the document, you won’t know it.

- You will need to validate the certificate manually (again outside your app’s workflow). It will probably take between 1 and 3 days to validate a bank account.

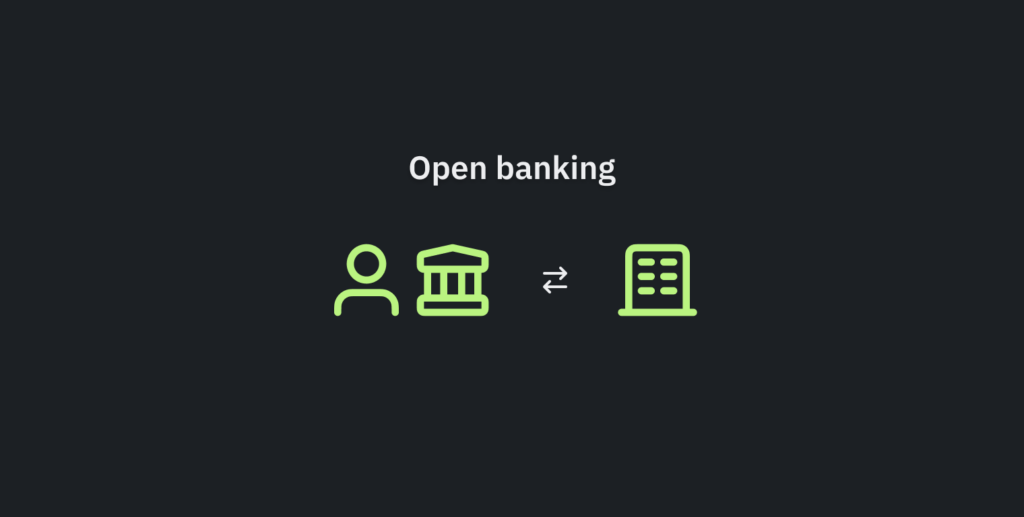

3. The user connects bank accounts with your system

The usage of open banking services for validating a bank account is a great method. Once you connect to an Account Information Service Provider (AISP), you can provide your users with a list of banks, they choose their bank and connect their account. That’s it, you receive the information of the bank account and their last statements.

Pros

- It’s fast, you will receive the name of the account’s holder immediately.

- It can be included in your application’s workflow.

- In case you need to create a financial profile of your customers it’s perfect, since you will be able to access all the products they have with this bank and also their last statements.

Cons

The main drawbacks here are:

- Corporate accounts are not always well supported by open banking providers.

- Your users worry about data overreach – full access to 12 months of bank transactions for 90 days just to verify the account holder feels excessive. Simpler, less invasive methods build trust and boost competitiveness.

- Finally, the price: It’s probably the most expensive option.

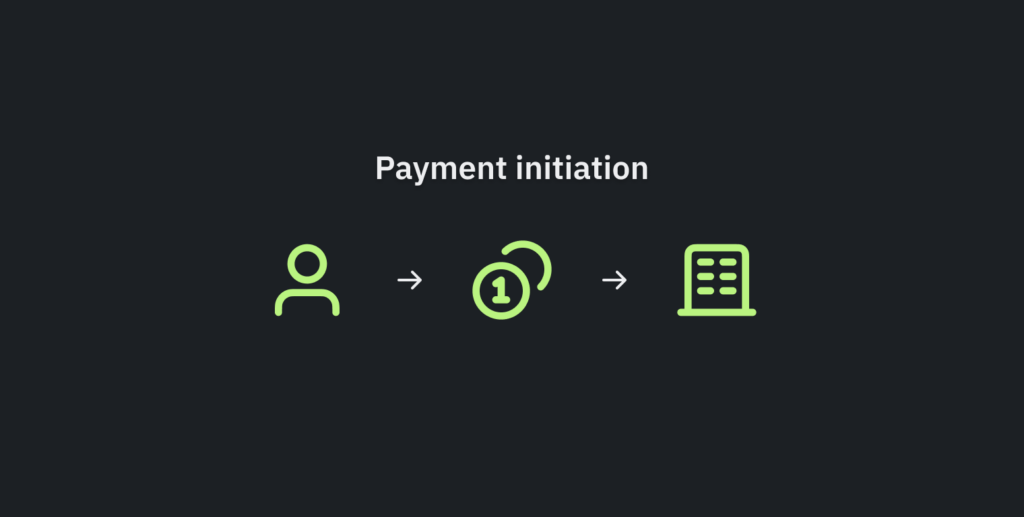

4. The user makes a micro-transaction and you check the data received

Asking your users to send you a small transaction is another method that can help you verify a bank account. If you do it using a payment initiation service provider (PISP) you can integrate verification into your workflow and do it 100% online. But this is not necessary, you can ask your users to do the transfer using their online banking.

Note: a PISP is a service to initiate account-to-account payments. Similar to seed ecommerce where you can pay with your bank account online in the same way you do with your credit/debit card.

Pros

- It’s probably the most complete method, since you are not just checking the ownership of the bank account but also that the person verifying the bank account can operate with it.

- In the case that you use a PISP, you can integrate this in your online processes for onboarding users.

Cons

- Its main pro is also a drawback, and you will need to explain to your users why they have to send money to you before becoming customers or decide what to do with the money once received.

- If your customer is a corporation, the payment can be tricky or even impossible, since the people with permission to execute payments are not always accessible at that moment and/or it could be more than one person.

5. You make a micropayment to your user and they verify a code

Sending a micropayment to your users and asking them to confirm the amount of a message in the description is the last method to verify a bank account and probably the most popular method up until recently.

Pros

- Traditionally it has been seen as a slow and offline process, which isn’t the case anymore. Instant payment APIs are very common and your users will receive the notification from their bank quicker than you might think.

- This method is not intrusive. Also, receiving money instead of being asked to pay or give you extra information is always a more comfortable experience for your users. This is especially effective if you want to verify bank accounts for collecting direct debits and not making payments.

Cons

- Only 99% of the banks in Europe support instant payments. So, there are a few users, those using small banks not supported yet, that won’t receive the money instantaneously.

- To be fair, what you are verifying here is that the user has access to the account, which is good enough in many cases but it might require other AML checks to be effective.

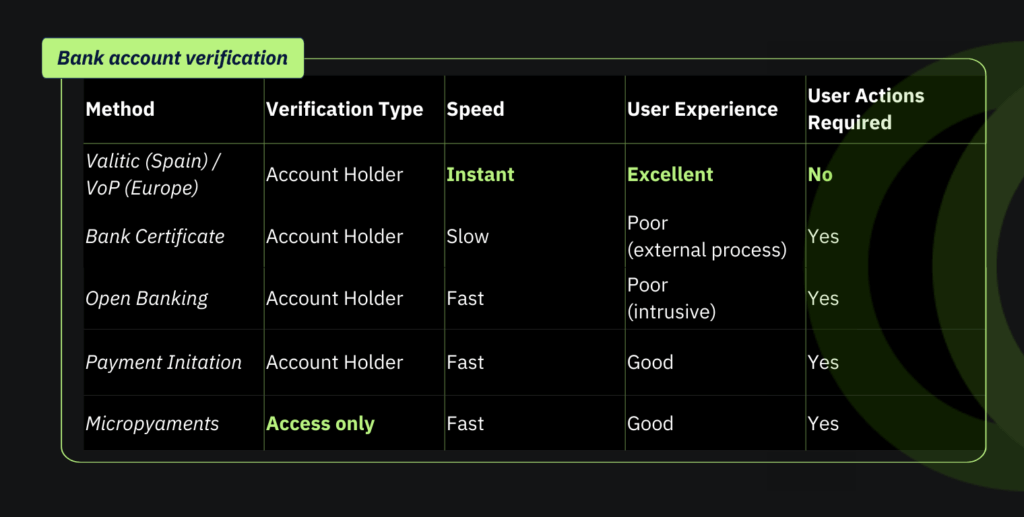

Comparison Table: Choosing the Right Method to Verify a Bank Account

How Devengo can help

Devengo offers two bank account verification methods that are easy to integrate via API:

Micropayment Verification

- Sends €0.01 with a verification code.

- Instant payments in 99% of cases.

- Immediate notification to the user.

Instant Verification (Valitic)

- Available in Spain.

- Real-time verification without user interaction.

- Instant IBAN-NIF/CIF/NIE matching.

With the arrival of the VoP (Verification of Payee) standard in October 2025, instant verification will become the European standard. Devengo is actively preparing for the integration of the VoP scheme.

Bonus point

As a payment service provider, Devengo informs you of the origin IBAN in micropayments, enabling dual verification that traditional banks do not offer.

Finally

Each method of bank account verification has its own pros and cons and it depends on your needs for which option to choose. Normally the account verification process is part of something larger, like building a profile or reduce fraud, so there is not a method that is the most recommended in all situations.

Not sure which method is best for your business? Request a call with one of our experts to explore the best option for you.